Frank dongyang/iStock via Getty photos

IntroductionKKR true estate Finance trust (NYSE:KREF) should record its Q1 consequences later this month however I'm not especially confident about how this 12 months will shape up for the loan investor. while the majority of the loans are senior loans with a floating activity cost, KREF had to focal point on damage handle these days as a few of the loans in its personal loan publication defaulted and required consideration. This most likely weighed on the results in 2022, and given the further increase of the activity costs on the market in 2023, KREF probably isn't out of the woods yet.

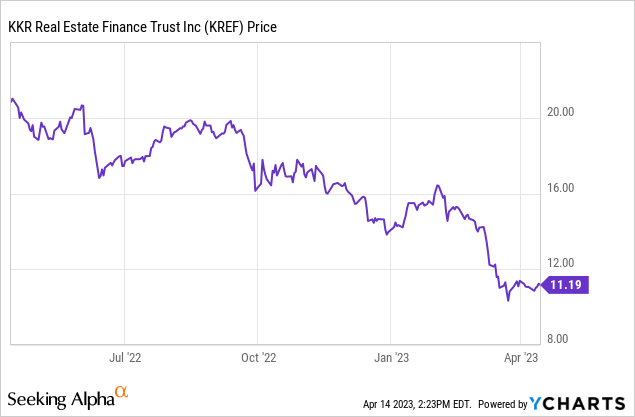

statistics with the aid of YCharts extra write-offs make the LTV ratios questionable

statistics with the aid of YCharts extra write-offs make the LTV ratios questionable however I'm more interested in seeing the distributable money movement calculation, we may still in fact birth with the earnings commentary as the internet income is the starting point for the DCF calculation.

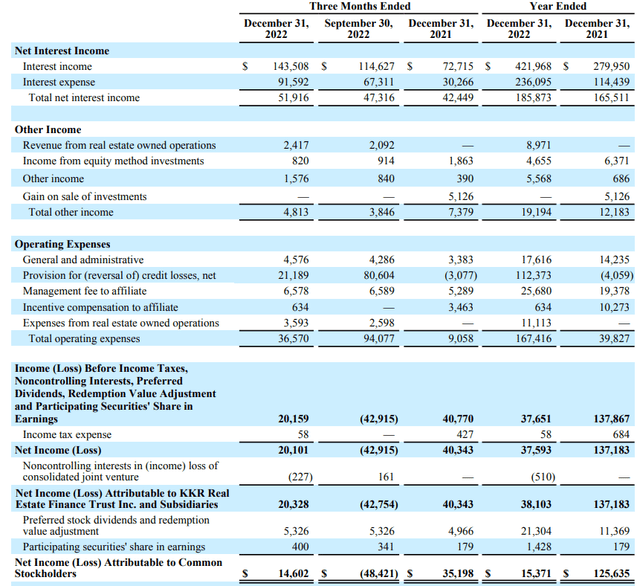

within the fourth quarter, KKR reported a total net pastime earnings of $52M. That's very encouraging as it shows the floating rate investments are paying off. while the REIT's interest prices improved through greater than a 3rd, the interest revenue elevated as neatly and the web activity earnings multiplied by using approximately 10% on a QoQ basis. to this point, so respectable.

KREF Investor family members

The leading challenge here is that the mortgage loss provisions remain excessive. a whole lot lessen than in Q3 2022, that's definitely authentic, but seeing a $21.2M personal loan loss provision absolutely nevertheless weighs on the underlying outcomes. The internet income got here in at $20.1M and after deducting the preferred dividends and the $0.4M payable to securities that participate in the internet salary, the bottom line showed a internet income of $14.6M for an EPS of $0.21.

whereas that's not dramatic considering the deserve to listing a loan loss provision of in extra of $21M, or not it's clear the salary don't cowl the present quarterly dividend of $0.forty three per share. And the fourth quarter wasn't a fluke. The FY 2022 web income became about $0.23/share due to a $112M+ loan loss provision.

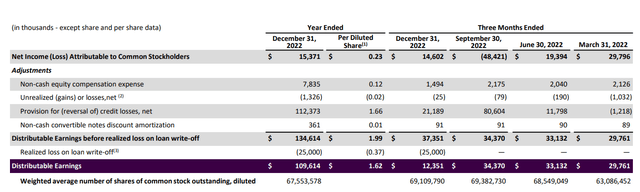

Of direction the REIT refers back to the distributable money circulation because the loan loss provisions are a non-money point. The distributable earnings add back the total personal loan loss provisions and best deduct the exact write-offs. As you could see beneath, this had a bad have an effect on on the this autumn result because the distributable profits were simply $12.4M or $0.18/share but the $25M write-off in this autumn become the best write-off right through the year.

KREF Investor relations

This skill the distributable revenue for FY 2022 were nonetheless a extremely first rate $109.6M or $1.62 per share using the weighted normal share count (and approximately $1.59/share the use of the valuable share count number).

That's nonetheless fairly respectable but the main question is how a ways KKR is kicking the can extra down the highway. possibly we should have a glance at why and the way the $25M write-off turned into realized. the clicking free up provides an excellent rationalization:

In January 2023, the enterprise achieved the amendment of a senior workplace loan discovered in Philadelphia, PA, that changed into risk-rated 4 at September 30, 2022, with an excellent predominant steadiness of $161.0 million, of which $25.0 million changed into deemed uncollectible and written off, as of December 31, 2022. The phrases of the modification protected, among others, a $25.0 million fundamental compensation and a restructure of the company's $136.0 million senior mortgage (after the $25.0 million compensation) into a $116.5 million dedicated senior personal loan loan (including future funding of $5.5 million) and a $25.0 million junior mezzanine notice

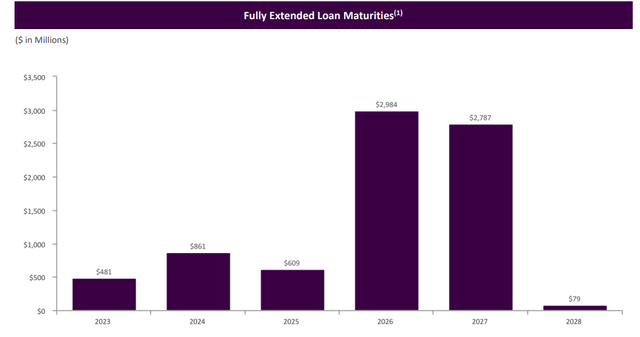

whereas it's fantastic to look the REIT has been able to come to an settlement in preference to being handed the keys, it does carry some question marks here. in response to the Q3 2022 corporate presentation, the $161M loan had an legitimate LTV ratio of 72%. whereas that's no longer foremost, it ability the fair price of the collateral changed into estimated at about $220M. In thought that's first-class. but seeing how KREF has to take a haircut on a senior personal loan makes me somewhat fearful about its publicity to the office portfolio as this basically wasn't the first fireplace KREF needed to put out. In my outdated article, I discussed there are extra loans maturing this year that may require an extended-term answer.

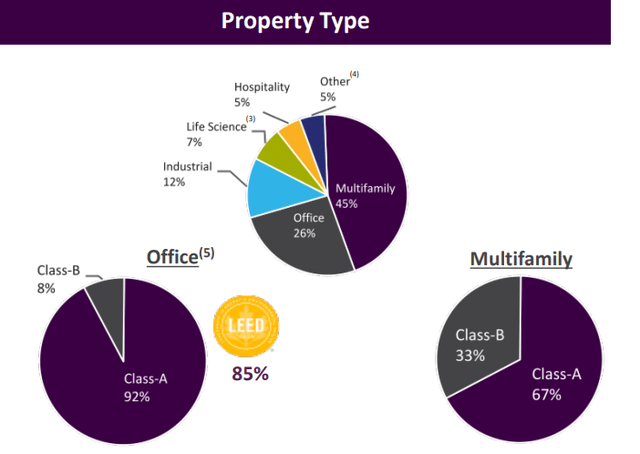

fortunately I actually have the affect KREF is aware this risk. first off, the office portfolio represents just 26% of the asset base (however creates near one hundred% of the complications) so so long as the portfolio of multifamily property performs neatly, the fallout from a deteriorating local weather in the workplace phase should still and could be coated.

KREF Investor relations

Secondly, the brand new loans KREF has funded right through the fourth quarter appear to have a lots lessen possibility profile. The normal LTV ratio is simply 58% and all three loans are non-workplace loans. There are two multifamily loans and a self-storage personal loan and the general money coupon is at present approximately eight% (in keeping with the yr-end condition and the ordinary markup of 370 groundwork elements on the SOFR benchmark price).

KREF Investor family members

moreover, KREF expects $1B in repayments this year, peculiarly weighted in opposition t the second half of this year. that might be spectacular news because it will permit KREF to continue its greater conservative underwriting coverage.

KREF Investor members of the family

It's additionally essential to know that the belongings used as collateral for two other troubled loans which can be maturing this 12 months are at present in the income technique. From the this fall conference name:

related to our other two chance-rated 5 loans, there are sponsor-led sale procedures in growth, and we're maintaining an active talk with these sponsors. With the Minneapolis personal loan, we accomplished a short-term extension to facilitate the sale method. And for the different Philadelphia personal loan, we now have an initial maturity date in may additionally of this year.

funding thesisThere is generally more hits to the distributable profits within the present fiscal yr. In 2022, KREF recorded in extra of $112M in personal loan loss provisions but this doesn't affect the distributable earnings calculation except those losses materialize. In FY 2022 handiest $25M of these losses comfortably materialized. i am hoping to peer more details in the Q1 replace later this month and fortuitously the larger net activity revenue might be effective to absorb additional write-offs.

In my outdated articles I peculiarly focused on the favorite shares (trading with (KREF.PA) as ticker image) and i will update my view on the favorite shares after the Q1 effects. The favored dividends are nevertheless smartly lined, the ordinary share dividends basically weren't in 2022 and it remains to be viewed if the $0.43 quarterly dividend on the ordinary shares might be covered this 12 months. From a longer-term perspective, KKR is likely in a higher shape because it can now lend money at more positive terms than before.

0 Comments